All Categories

Featured

Table of Contents

[/image][=video]

[/video]

If you're in healthiness and happy to undergo a medical examination, you might get approved for typical life insurance policy at a much lower price. Surefire issue life insurance policy is typically unneeded for those in good wellness and can pass a clinical exam. Because there's no clinical underwriting, even those healthy pay the same costs as those with wellness concerns.

Given the lower insurance coverage amounts and greater costs, assured issue life insurance policy may not be the most effective choice for lasting monetary preparation. It's typically a lot more matched for covering last expenditures instead of changing earnings or considerable financial obligations. Some guaranteed problem life insurance policy policies have age limitations, typically limiting candidates to a specific age variety, such as 50 to 80.

Assured issue life insurance comes with greater premium prices compared to clinically underwritten plans, but prices can differ dramatically depending on factors like:: Various insurance business have various pricing designs and might offer various rates.: Older candidates will pay greater premiums.: Women frequently have reduced prices than males of the exact same age.

: The survivor benefit amount impacts premiums. A $25,000 plan prices less than a $50,000 policy.: Paying premiums month-to-month expenses much more total than quarterly or yearly payments.: Entire life costs are greater general than term life insurance policy policies. While the assured issue does come at a cost, it gives vital coverage to those that might not get generally underwritten policies.

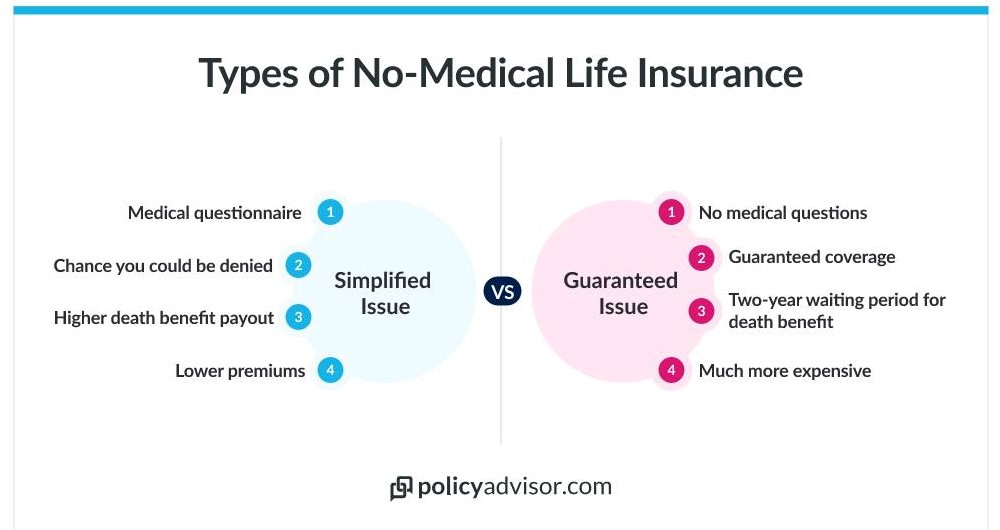

Surefire concern life insurance policy and simplified problem life insurance policy are both kinds of life insurance policy that do not need a clinical exam. There are some important distinctions between the two types of plans. is a sort of life insurance policy that does not need any kind of health and wellness inquiries to be answered.

What Is An Instant Life Insurance Policy? for Beginners

Guaranteed-issue life insurance plans typically have greater costs and reduced death benefits than conventional life insurance coverage plans. is a type of life insurance policy that does need some health and wellness questions to be responded to. The health and wellness concerns are usually less thorough than those requested conventional life insurance policy plans. This suggests that simplified issue life insurance policies may be available to individuals with some health issues.

Immediate life insurance policy coverage is protection you can obtain an immediate answer on. Your policy will certainly start as quickly as your application is accepted, meaning the entire procedure can be done in much less than half an hour.

Instantaneous protection just uses to term policies with sped up underwriting. Second, you'll require to be in really excellent health and wellness to qualify. Several sites are promising immediate protection that begins today, yet that does not imply every applicant will certify. Usually, consumers will certainly submit an application assuming it's for instant insurance coverage, only to be consulted with a message they require to take a medical examination.

The very same information was after that used to accept or deny your application. When you use for an accelerated life insurance coverage plan your information is evaluated quickly.

You'll then obtain immediate authorization, split second denial, or observe you need to take a medical examination. You might require to take a clinical test if your application or the information pulled concerning you reveal any kind of health and wellness problems or problems. There are numerous choices for instantaneous life insurance policy. It is necessary to note that while numerous conventional life insurance firms offer accelerated underwriting with rapid approval, you may need to experience a representative to apply.

The Basic Principles Of Life Insurance, No Medical Exam Options - Life Benefits

The companies listed below deal completely online, user-friendly options. The firm uses versatile, instant plans to people between 18 and 60. Ladder policies enable you to make adjustments to your coverage over the life of your plan if your requirements alter.

The firm uses plans to applications in between 21 and 55 for a ten-year term, and between 21 and 45 for a 20-year term. You'll get an instant choice from Bestow. There are no medical examinations required for any applications. Principles plans are backed by Legal and General America. The firm does not provide plans to locals of New York state.

Similar to Ladder, you might need to take a medical examination when you look for protection with Principles. Nonetheless, the company says that the bulk of applicants can get coverage without an exam. Unlike Ladder, your Values plan will not begin as soon as possible if you need an exam. You'll need to wait up until your exam outcomes are back to get a cost and acquire insurance coverage.

In other situations, you'll require to provide more information or take a medical examination. Right here is a rate contrast of insant life insurance coverage for a 50 year old male in excellent health and wellness.

A lot of people begin the life insurance policy buying plan by obtaining a quote. Allow's claim you got a quote for $50 a month for a $500,000, 20-year plan.

You can set the precise insurance coverage you're using for and after that begin your application. A life insurance policy application will ask you for a great deal of info.

Some Ideas on Best Life & Burial Insurance With No Waiting Period In 2025 You Should Know

It is very important to be 100% straightforward on your application. If the business finds you didn't divulge info, your plan might be denied. The decrease can be shown in your insurance score, making it more difficult to get coverage in the future. Once you send your application, the underwriting formula will assess your info and pull data to come to an instantaneous decision.

A simplified underwriting plan will ask you comprehensive inquiries about your clinical background and recent clinical care throughout your application. An instant problem plan will do the exact same, yet with the distinction in underwriting you can get an instant choice.

Second, the coverage quantities are reduced, but the costs are commonly greater. Plus, guaranteed concern policies aren't able to be used throughout the waiting period. This indicates you can't access the full fatality advantage quantity for a collection amount of time. For the majority of plans, the waiting period is two years.

Yes. If you remain in healthiness and can certify, an instant problem plan will certainly allow you to obtain insurance coverage without exam and no waiting period. What happens if you're in less than best health and desire a policy without any waiting duration? In that situation, a streamlined problem policy without any test could be best for you.

All about Can You Get Life Insurance Without A Medical Exam?

Remember that streamlined issue plans will certainly take a few days, while immediate policies are, as the name suggests, split second. Acquiring an instantaneous policy can be a rapid and very easy procedure, but there are a couple of things you ought to watch out for. Before you strike that acquisition button make certain that: You're getting a term life plan and not an unintentional death policy.

They do not supply protection for disease. Some firms will certainly issue you an unintended death plan instantly however require you to take an exam for a term life policy. You've checked out the small print. Some websites have lots of vibrant pictures and strong promises. Make certain you review all the information.

Your agent has addressed all your questions. Simply like web sites, some representatives highlight they can obtain you covered today without going into detail or providing you the info you require.

{kind=link}

Table of Contents

Latest Posts

Some Known Details About How To Buy Life Insurance Without A Medical Exam

Not known Incorrect Statements About Best No-exam Life Insurance Companies

The Ultimate Guide To What Is No Medical Exam Life Insurance?

More

Latest Posts

Some Known Details About How To Buy Life Insurance Without A Medical Exam

Not known Incorrect Statements About Best No-exam Life Insurance Companies

The Ultimate Guide To What Is No Medical Exam Life Insurance?